In this article:

- Opening Answer

- SR&ED Tax Credit Canada (Quick Summary)

- What Is SR&ED in Canada?

- The Three Criteria CRA Uses to Evaluate Claims

- Who Qualifies for SR&ED in Canada?

- What Work Qualifies for SR&ED?

- What Does NOT Qualify

- How Much Is the SR&ED Tax Credit Worth?

- What Costs Can You Claim?

- When Can You Claim & Carry-Forward Rules

- Why SR&ED Claims Get Rejected

- Common Misconceptions

- FAQ

- Next Step

Opening Answer

If your business is building software, improving a product, or solving technical problems, you could recover 15% to 35% federally — and up to 43%+ when combined with Ontario provincial credits — through the SR&ED tax credit in Canada.

For example, a Canadian-controlled private corporation (CCPC) spending $250,000 on eligible R&D work could receive $87,500 to $107,500+ in combined federal and provincial tax credits, depending on the province and structure. Yet many first-time founders miss this entirely—not because they don’t qualify, but because they misunderstand what the program actually rewards.

SR&ED Tax Credit Canada (Quick Summary)

- Federal credit: 15%–35% (refundable for CCPCs)

- Provincial top-up: 3.5%–8% (Ontario), other provinces vary

- Combined rate (Ontario CCPC): up to 43%+ refundable

- Covers: salaries, contractors, materials, overhead

- Applies to: software, manufacturing, engineering, biotech, clean tech, food processing

- Key requirement: technological uncertainty + systematic investigation

- Annual program size: $3+ billion in tax incentives (CRA)

- Filing deadline: up to 18 months after fiscal year-end

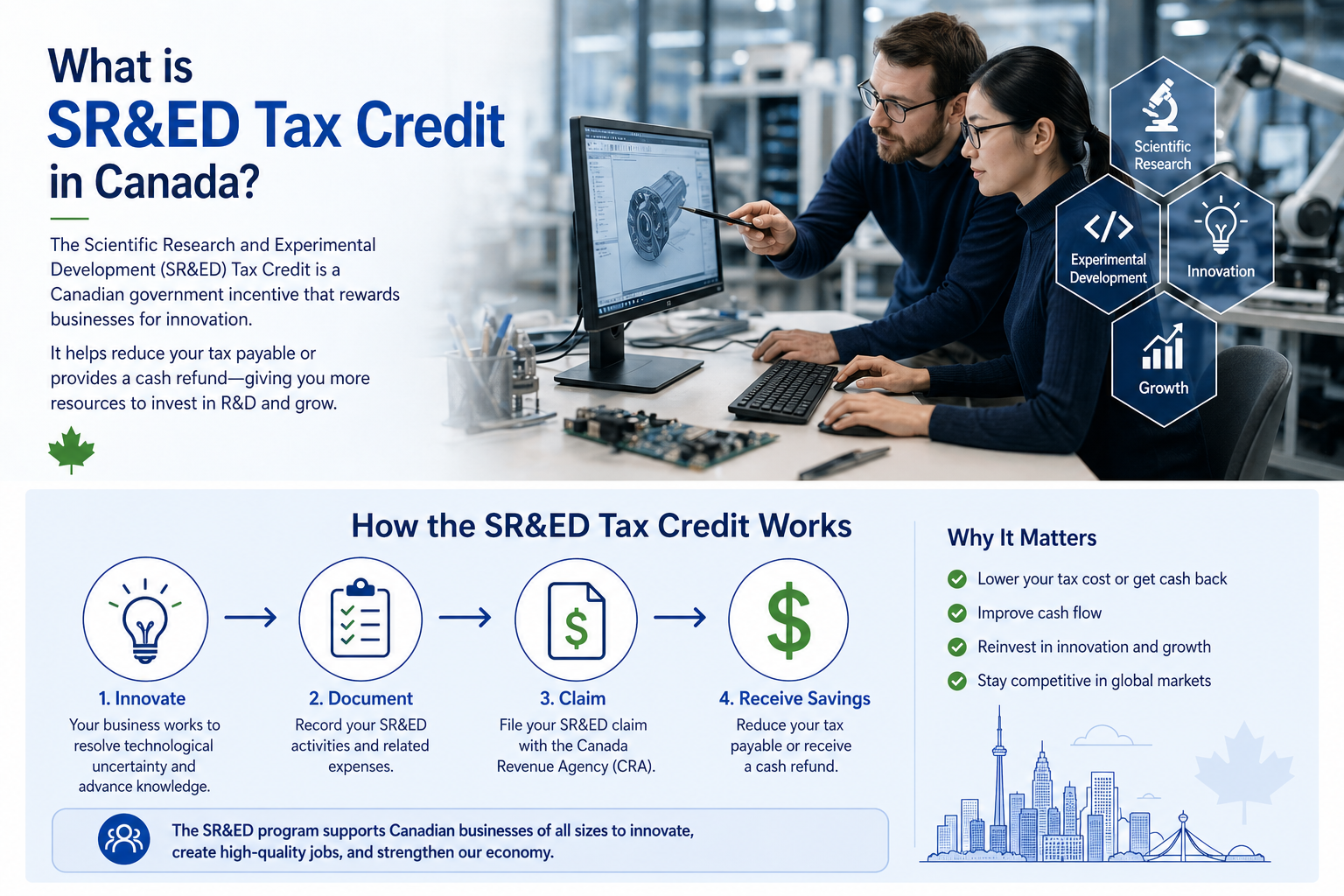

What Is SR&ED in Canada?

The SR&ED (Scientific Research & Experimental Development) program is the Canadian government’s largest single source of support for industrial R&D, administered by the Canada Revenue Agency (CRA). It provides over $3 billion in tax incentives annually to Canadian businesses across every sector.

It rewards businesses for attempting to solve scientific or technological problems—not just for building products. Eligible companies can claim both federal and provincial tax credits, with combined refundable rates reaching 43%+ for Canadian-controlled private corporations (CCPCs) in Ontario, and even higher in some other provinces.

This is the key distinction most founders miss:

SR&ED is not about innovation in a business sense—it’s about resolving uncertainty at a technical level.

From our experience working across industries, many valid claims are overlooked because teams assume their work is “just development”—when in reality, it involves unresolved technical constraints that meet SR&ED criteria.

The Three Criteria CRA Uses to Evaluate Claims

Every SR&ED claim must meet three criteria. CRA reviewers use these as a structured test to decide whether work qualifies—understanding them is the difference between a successful claim and a rejected one.

1. Technological Uncertainty

The work must address a technological problem that cannot be resolved through standard practice or routine engineering. The uncertainty must be technical in nature—not commercial, financial, or strategic. Standard caching, off-the-shelf APIs, or known engineering patterns don’t create technological uncertainty even if implementing them is complex.

2. Systematic Investigation

You must follow a structured, hypothesis-driven approach: form a technical hypothesis, design experiments, test under controlled conditions, measure results, and iterate. Trial-and-error without documentation, or implementation work that doesn’t test alternatives, won’t satisfy this criterion.

3. Technological Advancement

The work must aim to achieve new technological knowledge—knowledge that advances the understanding of how something works, even if the project itself fails commercially. Importantly, the advancement only needs to be new to your team or to publicly available knowledge, not new to the world.

For deeper guidance, review our SR&ED eligibility guide to see how the CRA applies these criteria in practice.

Who Qualifies for SR&ED in Canada?

SR&ED is not limited to large corporations or research labs. Eligible claimants include:

- Startups and early-stage companies

- Small and medium-sized businesses

- Established corporations

- Individuals and partnerships

What matters is the work performed—not company size or revenue. SR&ED claims have been successfully filed across software development, manufacturing, engineering, life sciences, clean technology, food processing, agriculture, and many other sectors.

The Practical Eligibility Test

Ask yourself:

- Was there a real technical unknown? (e.g., “We didn’t know if this architecture would scale under load.”)

- Did you try to solve it through experimentation? (not just implementation)

- Did you learn something new—even if it failed?

If yes to all three, you may qualify. The eligibility test is about the nature of the technical problem and the process used to resolve it—not the commercial outcome.

What Work Qualifies for SR&ED? (With Examples)

Most qualifying work falls under experimental development—where businesses attempt to overcome technological limitations. Here are realistic SR&ED examples drawn from claims we’ve prepared:

1. Software Performance Under Load

A SaaS company tried to reduce API response times under heavy concurrency.

- Standard caching and scaling failed

- Bottlenecks appeared unpredictably across tenants

- Engineers tested multiple concurrency models and measured failure states

👉 This qualifies because the uncertainty was technological, not just architectural preference.

2. Manufacturing Process Instability

A manufacturer struggled to maintain precision under fluctuating temperatures.

- Standard machine settings failed

- Engineers ran controlled trials adjusting cooling and feed rates

- Results were inconsistent and required iterative testing

👉 This goes beyond routine optimization—this is process-level uncertainty.

3. Formulation and Shelf Stability

A company attempted to stabilize a product without degrading performance.

- Existing methods didn’t predict outcomes

- Multiple formulations were tested under varying conditions

- Failures provided key insights

👉 Even failed attempts can qualify if they generate technical knowledge.

4. Hardware + Firmware Integration

A device company faced inconsistent sensor readings in real-world conditions.

- Issue wasn’t solvable with standard calibration

- Engineers tested signal noise, timing, and firmware adjustments

- Multiple iterations required to isolate root causes

👉 This is classic technological uncertainty SR&ED.

What Does NOT Qualify

Understanding exclusions is critical:

- Routine coding or feature development

- UI/UX improvements and aesthetic design changes

- Standard debugging

- Market research and sales promotion

- Routine quality control and testing

- Routine data collection

- Commercial production and operations

- Social sciences and humanities research

- Straightforward scaling using known solutions

The difference is subtle but critical:

- ❌ “We improved performance”

- ✅ “We attempted to resolve unpredictable latency caused by system-level constraints not addressed by known methods”

For more real-world breakdowns, see our case studies.

How Much Is the SR&ED Tax Credit Worth?

SR&ED provides both a tax deduction and a tax credit. The credit can be refundable (paid in cash even if you owe no taxes) or non-refundable (applied against future taxes). The rate depends on company type, expenditure level, and province.

Federal Tax Credit Rates

| Company type | Expenditure tier | Rate | Refundable? |

|---|---|---|---|

| CCPC | First $3M of qualifying expenditures | 35% | Yes (cash refund) |

| CCPC | Expenditures over $3M | 15% | No (carry forward) |

| Other corporations | All expenditures | 15% | No (carry forward) |

Ontario Provincial Top-up

| Credit | Rate | Refundable? |

|---|---|---|

| Ontario Innovation Tax Credit (OITC) | 8% | Yes, for qualifying CCPCs |

| Ontario R&D Tax Credit (ORDTC) | 3.5% | No |

| Combined Federal + Ontario (CCPC, refundable) | 43%+ | Yes |

Other provinces—Quebec, BC, Alberta, Manitoba, Saskatchewan, New Brunswick, Newfoundland, Nova Scotia, PEI—also offer SR&ED top-up credits with rates and refundability rules that vary. Quebec in particular has historically been one of the most generous.

Real Claim Value Examples

| Eligible Spend | Federal Only (Other Corp) | Federal Only (CCPC) | Federal + Ontario (CCPC) |

|---|---|---|---|

| $100,000 | $15,000 | $35,000 | $43,000+ |

| $250,000 | $37,500 | $87,500 | $107,500+ |

| $500,000 | $75,000 | $175,000 | $215,000+ |

| $1,000,000 | $150,000 | $350,000 | $430,000+ |

Key benefit for early-stage companies: CCPCs receive refundable tax credits even if the business has no taxable income. This means SR&ED can return real cash to your bank account—not just reduce future taxes.

What Costs Can You Claim?

SR&ED claims cover four main categories of expenditure. In most claims, labour is the largest contributor.

Salaries & Wages

Compensation for employees directly engaged in or directly supervising SR&ED activities. This includes developers, engineers, scientists, technicians, and project managers—to the extent their time was spent on eligible work. Time tracking and contemporaneous documentation matter here.

Materials

Cost of materials consumed or transformed during SR&ED—including prototypes scrapped during testing, test consumables, or production materials destroyed in experimental runs.

Contracts

Payments to arm’s length contractors for SR&ED performed on your behalf in Canada. Foreign contractor work is generally not eligible. Contractor SR&ED is typically claimed at 80% of the invoice amount.

Overhead (Proxy or Traditional)

You can either calculate overhead directly (traditional method) or use a CRA-prescribed proxy: 55% of eligible salary cost. Most claimants use the proxy method because it’s simpler and often more favourable.

To avoid under-claiming, it’s important to understand the full SR&ED claim process before filing. If you’re unsure how this applies to your business, explore industries we serve to see how claims vary by sector.

When Can You Claim & Carry-Forward Rules

SR&ED has favourable timing rules that many first-time claimants don’t realize:

- 18-month filing window: You can file SR&ED claims for up to 18 months after the end of your fiscal year. If you’ve been doing R&D but haven’t claimed before, you may still be able to file for the prior fiscal year. After 18 months, the right to claim is permanently lost.

- Carry-back (non-refundable credits): Unused non-refundable credits can be carried back 3 years to recover taxes paid in earlier years.

- Carry-forward (non-refundable credits): Unused credits can be carried forward up to 20 years, providing long-term tax savings even if you can’t use them immediately.

- Refundable credits: CCPC refundable credits don’t need to be carried—you receive them as cash from CRA, regardless of taxable income.

Why SR&ED Claims Get Rejected

This is where many first-time claims fail:

- No clear technological uncertainty

- Work described as business improvement rather than technical experimentation

- Weak or missing contemporaneous documentation

- No structured experimental process—just trial-and-error

- Technical narrative doesn’t match the financial claim

- Time tracking absent or estimated retroactively

The biggest issue is rarely actual eligibility—it’s how the work is framed and documented. Most rejected claims would have qualified if the project had been scoped, tracked, and described correctly from the start.

Common Misconceptions

“We need to be profitable”

False. CCPC refundable credits are paid in cash even with zero taxable income. Many SR&ED claims come from pre-revenue startups.

“We need a patent”

Incorrect. SR&ED rewards technical learning, not intellectual property. You can claim work that produces no patent, no product, and no IP.

“Only lab work qualifies”

No—software, manufacturing, and engineering work often qualify. The vast majority of SR&ED claims today come from software companies.

“If it failed, it doesn’t count”

Wrong. Failure often strengthens a claim if it shows real experimentation. The CRA explicitly accepts that uncertainty includes the possibility of failure.

“It’s only for big companies”

The opposite—the highest credit rate (35% refundable) is reserved for CCPCs, which are typically smaller. Larger non-CCPC corporations get a 15% non-refundable rate.

FAQ

What is SR&ED tax credit Canada in simple terms?

It’s a federal incentive that refunds 15%–35% of your costs (plus provincial top-ups, up to 43%+ combined for Ontario CCPCs) when you attempt to solve technical problems through systematic experimentation. CCPCs receive it as cash; other corporations get it as a tax credit they can carry forward.

Who qualifies for SR&ED in Canada?

Any Canadian business performing eligible R&D work—regardless of size, sector, or profitability. The work, not the company, determines eligibility.

What industries qualify for SR&ED?

SR&ED is sector-agnostic. Common claimants include software development, manufacturing, engineering, life sciences, clean technology, food processing, and agriculture. The key is the nature of the work, not the industry.

Can I claim for work done in previous years?

Yes—up to 18 months after your fiscal year end. Many companies discover SR&ED a year into a project and successfully file for the prior fiscal year. After 18 months, the right to claim is permanently lost.

Do I need to be profitable to claim?

No. CCPCs receive refundable credits as cash even with no taxable income. This is one of SR&ED’s most valuable features for early-stage companies.

What happens if my claim is audited?

CRA reviews a portion of SR&ED claims each year. If your claim is selected, the reviewer will request documentation of the technical work, time tracking, and financial calculations. Well-prepared claims with contemporaneous documentation pass review without issue. Henderson provides full audit defense at no additional cost on claims we prepare.

Does routine development qualify?

No—unless the routine development encountered a genuine technical uncertainty that required experimentation to resolve. The line between “routine” and “SR&ED” is exactly where most claims succeed or fail.

How much can I claim?

Typically 15%–35% federally on eligible costs, plus provincial top-ups bringing the combined refundable rate to as high as 43%+ for Ontario CCPCs. Other provinces have different rates.

Next Step

If you’re unsure whether your work qualifies, that’s exactly where most companies lose money.

We regularly see businesses:

- Miss entire eligible projects

- Under-claim technical staff time

- Misclassify experimental work as “non-eligible”

- Miss the 18-month filing window for prior years

A focused SR&ED review will show:

- What actually qualifies (and what doesn’t)

- How much you can realistically claim

- Where you’re leaving money behind

- Whether prior years are still recoverable

Book a claim assessment with Henderson & Associates and get a clear answer before your next filing deadline. We work on contingency—no upfront cost, fees only on credits successfully recovered.